1. Why have an investment philosophy?

An investment philosophy represents a set of core beliefs about how investors behave and how markets work. To be a successful investor, you not only have to consider the evidence from markets, but you also have to examine your own strengths and weaknesses to come up with an investment philosophy that best suits you. Investors without core beliefs tend to wonder from strategy to strategy, drawn by anecdotal evidence or recent success, consequently creating transaction costs, triggering taxes, and incurring losses along the way. Investors with clear investment philosophies tend to be more consistent and disciplined in their investment choices.

Various international and South African studies confirm that investors seldom get the “market return”. As an example, US investors consistently earn lower returns than the market and the funds in which they invest. This gap in performance is known as the behavioural penalty, and it’s big and relentless. $100 invested in the S&P 500 in 1996 would have grown to $480 by the end of 2015. The average investor’s $100 would have grown to only $250. That is a 92% difference in return between staying invested and reacting to the market’s moods and emotions. Although this research is US-based, there is no reason to believe that investor behaviour in the rest of the world is any different.

Human nature is to blame for the average investor's underperformance compared to the market. Behavioural finance teaches us that investors are too often driven by emotion, including buying high and selling low, which can impact their long-term portfolio performance. By having a clearly articulated and well-considered financial plan which is supported by a well- considered investment philosophy, we can assist investors in generating market-related returns and not becoming a victim to the market’s moods and emotions.

2. Five elements of our investment philosophy

2.1 Cost

We believe in eliminating all unnecessary costs where possible. The effect of just one or two percent in additional fees and charges can have a dramatic effect on long-term investments. The Effective Annual Cost (EAC), expressed as a percentage of your investment amount, is a measure which has been introduced to allow you to compare the cost you incur when you invest in different financial products. Common fees applicable to investments are:

Investment Management Fees: These fees are paid to the fund managers who are responsible for portfolio construction, portfolio optimisation, risk management, stock research and selection, asset allocation, portfolio monitoring and reporting.

Advice Fees: These cover the cost of the initial advice in setting up and/or restructuring a client’s balance sheet and portfolio. There is an initial advice fee for the analysis, recommendations and implementation of the proposed strategy. There is an ongoing service fee which covers the cost of portfolio reviews, client servicing and all associated record keeping and compliance requirements.

Administration Fees: These fees cover the cost of administering the various investment products, pricing, statements, tax certificates and fund aggregation.

2.2 Asset Allocation

We believe that all clients should be exposed to a variety of asset classes, even clients with extreme risk profiles. We believe that optimal asset allocation remains the single most important driver of investment returns and is the best way to manage risks associated with investing. Asset allocation will be undertaken with a view to including as many uncorrelated assets in a client’s portfolio as possible, provided the final portfolio objectives reflect the investment objectives of the client.

2.3 Risk

We believe that investing entails risk. We define risk as the potential for permanent capital loss, and for not achieving a client’s investment objective. We also believe that risk only rewards up to a point, then it becomes destructive. Our approach to risk is to understand the risks associated with any particular investment strategy and to ensure that all diversifiable risk is managed through appropriate diversification. The aim of our risk management activities is to reduce the downside risk to client portfolios. The overall riskiness of a portfolio must always reflect the risk profile, risk tolerance and risk attitudes of the client.

2.4 Risk Tolerance

Understanding the clients’ tolerance for risk is a key part of formulating the investment objectives and deciding on an investment strategy. Our role is to fully understand the risk tolerance of the client and identify situations where there is a large gap between the clients’ risk tolerance and the risk profile of the investment strategy needed to meet the clients’ objective. Our challenge is to manage this gap and reduce it to a more acceptable level.

2.5 Tax Constraints and Considerations

We believe that the tax status of a client can have a major impact on the investment strategy adopted and that tax considerations will always be incorporated into the investment planning process. The goal of tax planning from an investment perspective will be to maximise after-tax returns, not to minimise taxes.

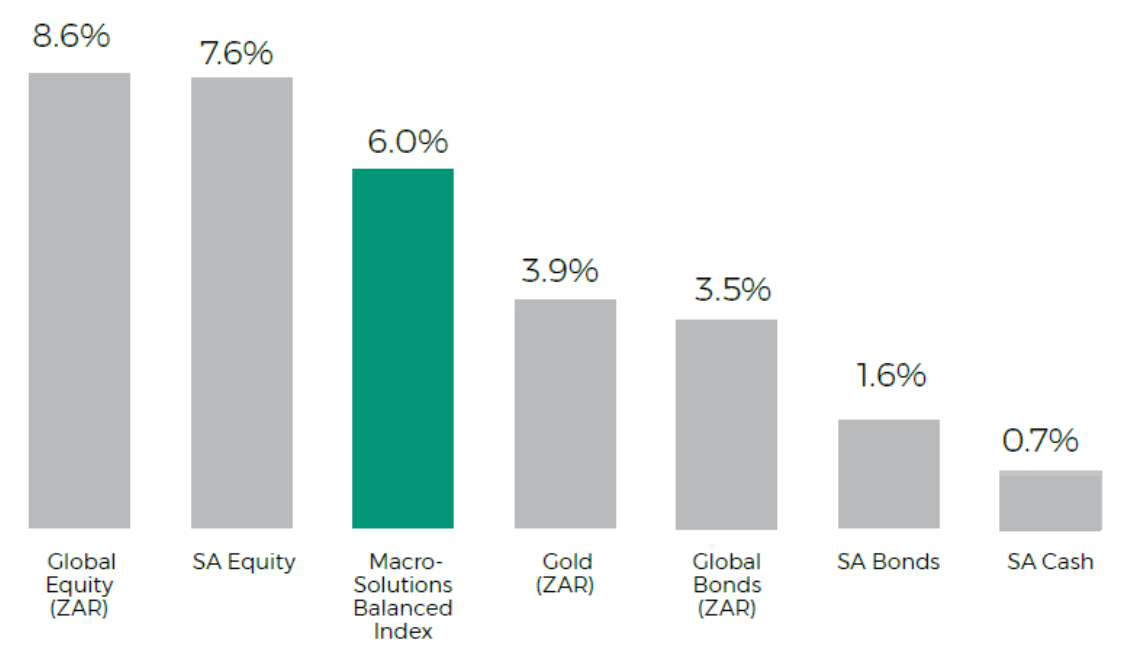

3. Available investment returns for South African residents

The below provides a summary of the opportunity in investing in South African and International assets in Rand terms. This provides some guidance on what the return is that can be generated by keeping the assets invested in South Africa or investing internationally. The below are real returns i.e. the returns available after taking into account inflation.

• Source: Old Mutual Investment Group

It is important to note that market returns are not delivered in a straight line, investors benefit from the above returns by staying invested in the market over the long term. Market corrections or crashes are not unusual and happen on average every 6 years. These cannot be timed, and it is important to stay invested to benefit from the spectacular returns after a crash and benefit from the long-term returns.